Discover the CapEQ approach to a premium exit

Whether you're exploring your options or fending off offers, we're here to help.

Published: July 2026 | Reading time: 9 minutes

UK payroll software M&A activity has reached its highest level in twenty-six years, sustaining the momentum built through the previous year, and comparable buy-and-build activity is playing out across the wider European market at the same time.

International strategics and private equity buyers are the dominant acquirer type on both sides of the Channel, drawn to scalable platforms with recurring revenue and a defensible compliance position. Regulatory change is accelerating consolidation on both markets — the UK's Employment Rights Act 2025 in Britain, and parallel compliance and labour-market legislation across the EU — as smaller vendors struggle to fund the compliance and automation investment that buyers now expect.

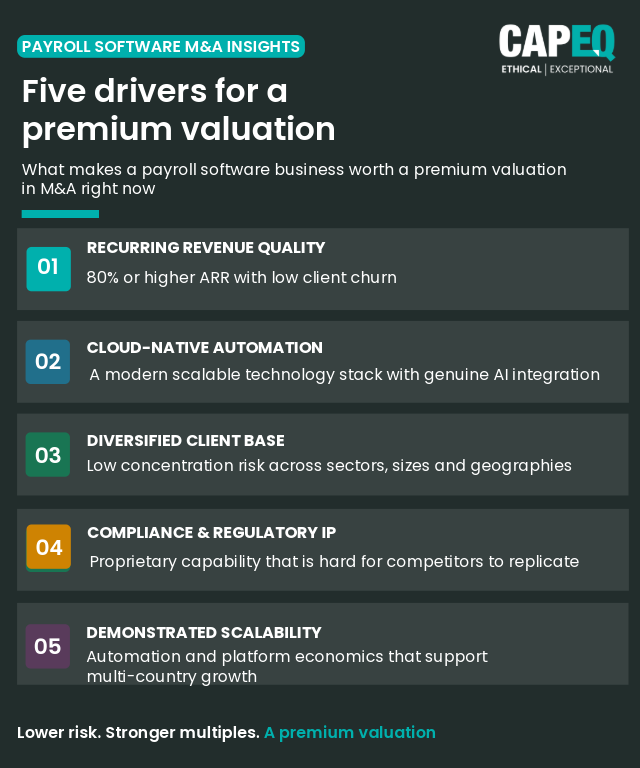

For founders, the takeaway is direct: buyer appetite is strong across the UK and Europe, but it is no longer indiscriminate. Premium valuations are reserved for cloud-native, highly automated platforms with diversified client bases and low key-person dependency, wherever in Europe they are based.

Legacy, on-premise, or founder-dependent businesses are transacting, but at a discount. Deal structures increasingly include earn-outs and rollover equity, reflecting genuine buyer conviction combined with a need to bridge valuation gaps created by automation and regulatory uncertainty. Founders considering an exit in the next one to three years should treat readiness — not market timing or geography alone — as the primary lever within their control.

Deal activity in UK payroll software is at its strongest point in more than two decades, and the same buy-and-build dynamic is visible across continental Europe. Three forces are compounding at once.

International acquirers — American and European alike — are moving on what they perceive as a valuation gap in UK and European technology assets.

Private equity continues to back buy-and-build strategies across the wider HCM services space, assembling platforms that span multiple European jurisdictions rather than staying within a single national market.

Regulatory change — the Employment Rights Act 2025 in the UK, alongside comparable compliance and labour-market legislation across the EU — is forcing a wave of compliance-driven platform investment that not every vendor can fund independently.

The result is resilient, arguably elevated, transaction volume across the region — concentrated on businesses with proven recurring revenue and a genuine digitalisation strategy already embedded.

Four patterns define the current market, consistently on both sides of the Channel:

| Trend | Description | What we are seeing |

|---|---|---|

| Consolidation | Smaller and family-owned vendors are exiting as owners retire and larger groups divest non-core suites | Ageing owner base; platform divestment activity across the UK and Europe |

| Buy-and-build | PE and trade acquirers are assembling UK and cross-border European payroll assets into pan-European or vertical-specific platforms | Comparable buy-and-build activity already visible among established European HCM groups |

| International and PE buyer dominance | Overseas capital and PE sponsors now lead deal count in both the UK and continental Europe | UK and European assets alike viewed as strategically undervalued and compliance-rich |

| Staged consideration | Earn-outs and rollover equity are now the norm, not the exception, across UK and European deals | Structures bridge valuation gaps tied to automation and regulatory change |

Buyers are paying a clear premium for defensible, recurring revenue, quality intellectual property, and demonstrable automation — a pattern consistent across the UK and European markets. Verified multiples for sub-£100m UK and European payroll software transactions are not widely disclosed, but the pattern across comparable deals is consistent.

Publicly disclosed UK and European payroll and HCM transactions point to mid-to-high single-digit EBITDA multiples as the general band, with high-growth, highly automated platforms commanding double-digit multiples from strategic or international acquirers. Trade divestitures and businesses running sunsetted legacy systems transact below these levels, regardless of geography.

The exit decision for most owners is not driven by a single factor, and the pattern holds across UK and European founders alike. It is the accumulation of six pressures, several of which are structural rather than cyclical:

CapEQ advised the shareholders of PayCaptain — the UK's first B Corp certified payroll provider — on its sale to compliance software group The Citation Group, completed in June 2026.

It's Citation's second payroll acquisition in 12 months, and founder Simon Bocca continues as Managing Director of the new Payroll Division. Read the deal story →

Direct UK and European payroll software platform transactions above £10m remain largely undisclosed for this period. Publicly reported UK and European SaaS and payroll M&A activity is dominated by international strategics and private equity platforms; the transactions below are the verified deals with clear UK or European relevance.

| Target | Target HQ | Deal type | Acquirer/investor | Value $m |

| Zalaris | Norway | Take-private | Norvester (NO) | 223 |

| Sona Technologies | UK | Series B raise | N47 (US) | 45 |

| Ordio | Germany | Series A raise | 3VC (AT) | 12 |

| Sloneek | Slovakia | Series A raise | Orbit Capital (CZ) | 6 |

| PayCaptain | UK | Acquisition | Citation Group (UK) | n/a |

| Paie & RH Solutions | France | PE bolt-on | SD Worx (BE) | n/a |

| Employes | Netherlands | PE bolt-on | Ageras (DK) | n/a |

| Socialea | France | PE bolt-on | SD Worx (BE) | n/a |

| Lohn AG | Germany | Acquisition | Mirus (CH) | n/a |

| Tamigo | Denmark | SBO | Accel KKR (US) | n/a |

Source: CapEQ analysis of publicly reported transactions, July 2025 – July 2026. Direct continental European transaction data is more limited in public disclosure than UK data; this table will be expanded as further verified deals are confirmed.

1. Deal volume will likely remain robust across the UK and Europe, but selectivity is intensifying around automation, compliance features, and client stickiness.

2. Buyer appetite stays strong, led by US private equity and global consolidators active in both markets, but buyers are becoming more discerning on technology quality and revenue durability.

3. Valuation trajectories are diverging. Premium multiples are increasingly reserved for cloud-native, automated platforms, wherever in the UK or Europe they are based. Legacy bolt-ons, sunset portfolios, and founder-dependent businesses will see a widening discount.

4. AI-driven automation will continue to compress legacy seat-based pricing models, which changes how buyers underwrite recurring revenue quality across both markets.

5. Regulatory change will keep raising the compliance bar — in the UK and across EU jurisdictions alike — and compliance capability will keep functioning as a valuation lever rather than a cost centre.

6. Deal structures will keep evolving, with earn-outs and staged consideration remaining standard rather than exceptional.

7. Early preparation will separate premium from average outcomes. Founders who address key-person risk, client concentration, and technology debt before going to market are positioned for the strongest valuations in a fast-moving market, regardless of which side of the Channel they are on.

CapEQ advised the founders of Paycircle, a cloud-native payroll platform built for UK bureaus, on its sale to The Access Group.

The deal was structured as 85% upfront consideration with the remaining 15% deferred over two years against ARR targets — a good example of how earn-outs work in practice in this sector. Read the deal story →

This report synthesises publicly reported UK and European payroll software and HCM transaction data, sector commentary, and CapEQ advisory analysis for the period July 2025 to July 2026.

Verified deal multiples for sub-£100m UK and European payroll software transactions are not consistently disclosed; indicative valuation ranges are derived from comparable, publicly reported HCM and SaaS transactions.

UK transaction data is more consistently disclosed than continental European data; where European-specific evidence was limited, this report draws on cross-border and pan-European buy-and-build activity as the clearest available indicator of the wider market.

Notable transactions are limited to publicly confirmed deals with clear UK or European relevance. This report does not constitute investment advice.

James Pugh is a Partner at CapEQ, the Certified B Corporation lower mid-market M&A advisory. He has led transactions across technology, healthcare, manufacturing, and professional services over a 15-year M&A career. Read his full bio or book a confidential chat.

Related insights:

What types of buyers are most active in UK and European payroll software M&A right now? The most active buyers are US private equity groups, international strategic software companies, and larger UK and European technology platforms pursuing buy-and-build expansion. Interest from overseas investors is being driven by a perceived valuation discount in UK and European assets and by scalable, recurring-revenue business models.

Which factors most influence the valuation of a payroll software business, in the UK or Europe? Key drivers include a high proportion of recurring revenue, a modern cloud technology stack, a diversified client base, automation and IP assets, low key-person risk, and regulatory compliance capability — whether that compliance capability is UK- or EU-specific. Client concentration and legacy technology reduce achievable multiples in both markets.

Why are so many UK and European payroll software founders exiting or seeking growth capital now? Reasons include founder retirement, the capital intensity of ongoing technology refresh, new regulatory burdens including the UK's Employment Rights Act 2025 and comparable EU legislation, competition from global platforms, and a genuine desire to de-risk personally. For many owners, a sale is the clearest route to securing value while supporting an orderly succession.

How are deal structures evolving in this sector? Earn-outs, staged consideration, and rollover equity are now standard across UK and European deals. These structures help align incentives after completion and bridge valuation gaps, with an increasing share of consideration linked to recurring revenue performance and automation delivery.

What is the single most important action for founders considering an exit, wherever they are based? Prepare early. Address key-person dependency, technology modernisation, and client concentration well before entering a process. Specialist M&A advice helps founders anticipate buyer questions, maximise achievable value, and avoid surprises in diligence, whether the process runs in the UK, Europe, or across both.

How is regulatory change affecting payroll software valuations across the UK and Europe? In the UK, the Employment Rights Act 2025 is accelerating demand for compliance-automation features and raising the ongoing investment bar for vendors. Comparable dynamics are playing out across EU jurisdictions as labour-market and compliance legislation evolves. Platforms that can demonstrate mature, embedded compliance capability are attracting a valuation premium in both markets; vendors reliant on manual or partial compliance processes are seeing that gap priced in as a discount.