Venture equity sells a stake in your company for capital, expertise and networks. Venture debt is a loan that sits alongside an equity round so you can grow without giving away more ownership. Most fast-growing UK businesses use both — equity to fund the leap, debt to extend the runway. The right mix depends on your stage, your cash flow and how much control you want to keep.

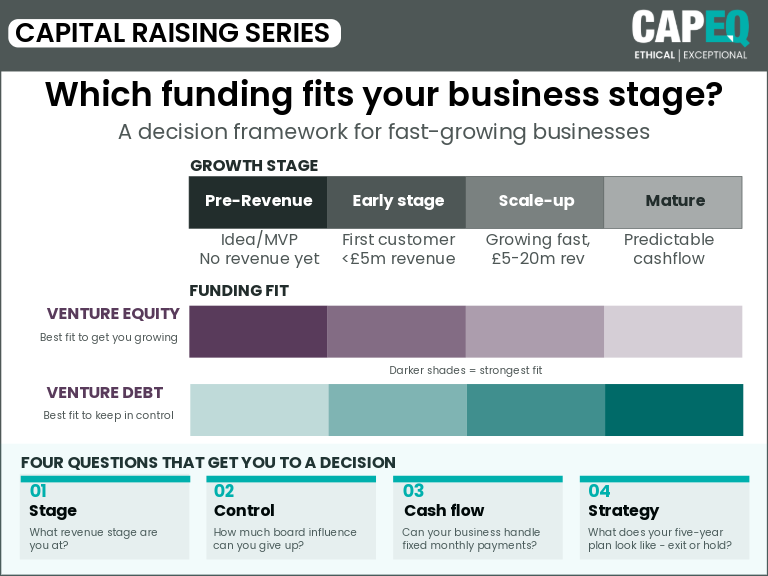

- Choose venture equity if: you are pre-revenue or pre-profit, you want a strategic partner, and dilution is an acceptable trade-off for speed.

- Choose venture debt if: you have £1m+ in revenue, strong intellectual property, and want to stretch an equity round without selling more shares.

- Most founders blend the two — and that is usually the smartest move.

What is the difference between venture debt and venture equity?

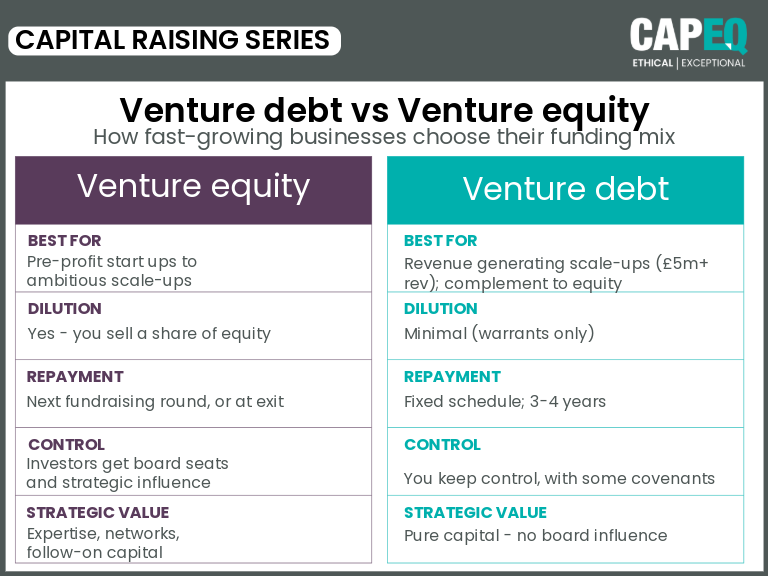

Venture equity is investment in exchange for shares. You sell a percentage of your company to venture capital, private equity or angel investors. They get ownership and influence; you get capital, expertise and a network. Repayment only happens at an exit.

Venture debt is a loan designed for high-growth companies. A specialist lender provides capital, you pay it back with interest over three to four years. You keep your shares. Lenders usually expect you to have already raised equity, have £5m+ in revenue, and own strong intellectual property.

Most founders we work with do not pick one or the other. They use both, sequenced thoughtfully, to fund the next stage of growth.

Venture equity: capital, partners, dilution

Selling equity in return for investment has been the mainstay of capital raising for decades. It has clear strengths — and one obvious cost.

What you gain

Expertise and networks. Good investors bring more than money. They open doors to customers, hires, future investors and acquirers. Where a partner-led approach really pays off is in the introductions you would never make on your own.

Long-term capital. No monthly repayments. No covenants to trip. You focus on growth instead of debt service.

Shared risk. Your investors only make money if you do. As a rule of thumb, venture capital tends to be more passive, while private equity is more demanding on governance and reporting.

What you give up

Dilution. You sell a slice of the company. That changes who decides what — at the board, on strategy, and at the exit.

Speed of decision. With investors at the table, big calls take longer. That is a feature, not a bug, but worth knowing before you sign.

Exit expectations. Equity investors need a liquidity event. Their timeline becomes part of yours.

What this looks like in practice

When our co-founder James Pugh advised the leadership team at Vegetarian Express through their growth investment from Bridges Ventures, the founders were clear on what they wanted: not just capital, but a values-aligned partner who understood their sustainability mission. The right equity partner did not just write a cheque — they backed a culture and a long-term plan. Read more about our approach to growth capital advisory.

Venture debt: keep your shares, take on a loan

Venture debt providers lend to start-ups and scale-ups that do not yet have positive cash flow or significant assets to use as collateral. Eligibility usually means demonstrably strong intellectual property and revenues above £1m. Pros and cons:

What you gain

Preserved ownership. No new shares issued, no further dilution. You and your existing shareholders keep what you have.

Flexible repayment. Most venture debt comes with interest-only periods and bullet payments at the end of the term. That gives you cash flow relief during the scrappy early stages.

A complement to equity. Venture debt sits neatly alongside equity. It can bridge funding gaps between rounds, fund a specific acquisition, or extend your runway long enough to hit the milestones that drive a higher valuation next time.

What you give up

Interest and fees. Venture debt is cheaper than equity in dilution terms, but it is not free. You will pay interest, fees, and sometimes warrants.

Covenants and reporting. Lenders want to see what is happening inside the business. Most venture debt does not require personal guarantees if the loan can be asset-secured, but expect tighter financial reporting and some restrictions on what you can do with the cash.

Cash flow pressure. A loan must be repaid. If your forecasts slip, debt service becomes a real constraint. Be honest about what your business can comfortably carry.

How to choose: venture debt or venture equity?

The honest answer is "it depends" — but there are four questions that get you to a clear-eyed decision.

Compare at a glance

| Factor | Venture Equity | Venture Debt |

|---|---|---|

| Best for | Pre-revenue or pre-profit start-ups; ambitious scale-ups | Revenue-generating scale-ups (£1m+); complement to equity |

| Cost of capital | Highest (you give up upside in shares) | Lower (interest and fees, sometimes warrants) |

| Dilution | Yes — significant | Minimal (warrants only, if any) |

| Repayment | At exit, via liquidity event | Fixed schedule, typically 3–4 years |

| Control | Investors get board seats and influence | You keep control, with some covenants |

| Speed to close | Months — complex due diligence | Weeks — simpler legal documentation |

| What lenders/investors want | Vision, market, team, growth potential | Strong IP, £1m+ revenue, prior equity backing |

| Strategic value | Expertise, networks, follow-on capital | Pure capital — no board influence |

1. What stage are you at?

Early-stage and pre-profit? Equity is usually the right answer. Investors take the risk, you get the runway and the expertise. Mature, with predictable cash flow? Venture debt may be the smarter, less dilutive choice.

2. How much control do you want to keep?

If giving up board seats and a slice of the upside makes you uncomfortable, venture debt protects ownership. If you genuinely want a strategic partner who will challenge your thinking, equity is the better fit.

3. Can your business comfortably handle repayments?

Venture debt is debt. Interest is due whether revenue grew this quarter or not. Stress-test your forecast. If a slow quarter would put debt service at risk, equity gives you more flexibility.

4. What does your long-term strategy look like?

Equity investors will expect a liquidity event — an exit or IPO — within a defined window. Venture debt has no such expectation. Think about the next five years, not just the next twelve months. (See our piece on exit strategy for your business.)

Common questions about venture debt and venture equity

-

Can I use venture debt and venture equity together? Yes — and most fast-growing companies do. Venture debt is usually structured to sit alongside equity, often raised within a few months of an equity round closing. A typical pattern is to add £2-3m of venture debt on top of a £10m equity raise to extend runway.

-

How much venture debt can I raise? Lenders typically offer 25–35% of your most recent equity round. So a £10m equity raise might support around £2.5–3.5m of venture debt.

-

Is venture debt cheaper than venture equity? In pure cost-of-capital terms, yes. You will pay interest and fees, but you keep the upside. Equity is the most expensive form of capital if your company succeeds — because the investors share in that success.

-

Do I need an existing VC investor to raise venture debt? Usually, yes. Venture debt lenders take comfort from a credible equity investor on the cap table. They are lending against the assumption that the next equity round will happen.

Next steps: finding your funding mix

Both venture debt and venture equity have real strengths. The question is rarely which one — it is which mix, in what sequence, on what terms.

That is the conversation we have most often with founders. We help you stress-test your plan, map it against current investor and lender appetite, and build a capital strategy that matches your growth ambitions, your risk tolerance and your long-term vision.

CapEQ helps business owners navigate the investment world to secure capital for growing companies. We are a certified B Corporation — so when we say "ethical, exceptional", that is what is on the tin.

Book an intro call with Douglas Edmunds to talk through your options.

Related insights

- Smart capital: when to raise venture debt (Growth Capital series)

- Unlocking growth: how to choose the right funding for your business (Growth Capital series)