Discover the CapEQ approach to a premium exit

Whether you're exploring your options or fending off offers, we're here to help.

Due diligence can stall or sink a sale; here is how UK founders prepare data rooms before buyers start digging.

Series: Business sale process · Business Sale Process Unpacked · Last updated: July 2026

The Gist

- Due diligence is the buyer's verification process, not a formality — it checks that every claim made during marketing holds up under evidence.

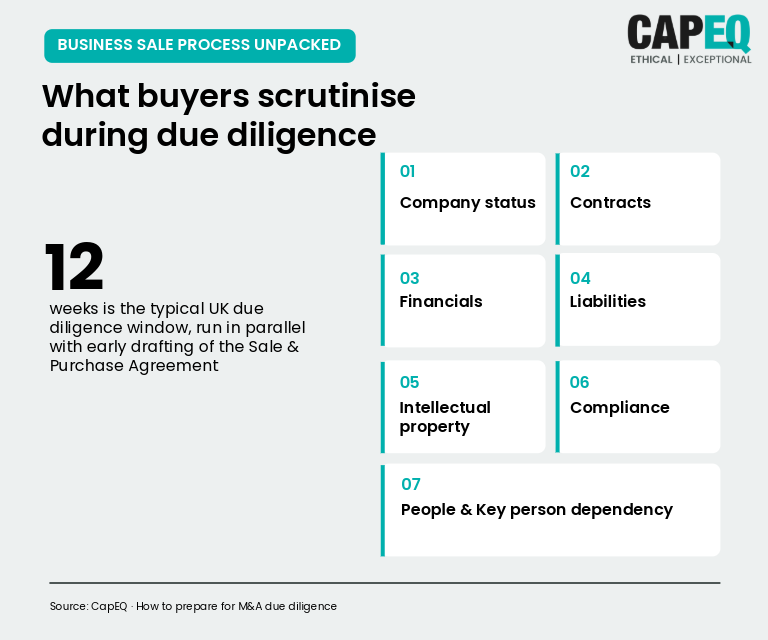

- Most SME due diligence covers seven areas: company status, contracts, financials, liabilities, intellectual property, compliance, and people.

- A significant number of CapEQ clients who prepare their data room before going to market complete their sale with fewer renegotiations and less delay.

- The single biggest cause of a repriced deal is disorganised or missing documentation, not a genuinely bad business.

- Preparation does not guarantee a higher price. It protects the timeline, the terms, and the buyer's confidence in what they are agreeing to.

Due diligence — two words that unsettle even confident founders. Boiled down, it simply means answering a buyer's questions with evidence rather than assurance.

A buyer who has agreed heads of terms has already decided, in principle, that they want your business. Due diligence is where they check that the business they are buying matches the business you described. It is the gap between "I believe you" and "I can prove it."

That gap is where deals slow down, reprice, or fall apart entirely.

Due diligence is the structured investigation a buyer (and their advisers) carries out between agreeing heads of terms and completing a transaction. It exists to verify the facts behind the price: the numbers, the contracts, the ownership, the risks.

People often compare it to the disclosures a homebuyer receives from a seller's conveyancer. The comparison breaks down quickly. A house buyer wants to know what is included in the sale and whether the boiler works. A business buyer needs to understand who your customers are, how dependent the business is on you personally, what your intellectual property actually belongs to, and whether your accounts will withstand scrutiny.

The result is a far deeper, far slower process than most founders expect — and one that consistently exposes the same gap: information exists, but it is outdated, scattered across inboxes, or was never written down at all.

The earlier you start compiling it, the less that gap costs you later.

Every due diligence process is tailored to the specific business and sector, but SME deals in the UK tend to converge on the same seven categories. Each maps to a different part of the buyer's risk assessment.

| Category | What buyers are checking | What "prepared" looks like |

|---|---|---|

| Company status | Incorporation certificates, shareholder register, share history | Companies House filings current; register matches reality |

| Contracts | Customer and supplier terms, change-of-control clauses | Signed copies on file; key contracts summarised |

| Financials | Revenue quality, add-backs, three-year trend | Management accounts reconcile to filed accounts |

| Liabilities | Borrowings, pensions, insurance, leases | Full schedule of obligations, nothing "off-book" |

| Intellectual property | Ownership of trademarks, code, and domain assets | IP formally assigned to the company, not an individual |

| Compliance | Litigation history, regulatory permissions, GDPR | No undisclosed disputes; policies documented |

| People | Contracts, key-person dependency, TUPE exposure | Employment records complete; succession plan for founder tasks |

The pattern across all seven is the same. Buyers are not looking for a perfect business. They are looking for a business that can explain itself.

When CapEQ advised on the sale of a construction manufacturer, the sector's typical due diligence pinch points — equipment condition, supplier contracts, environmental compliance — were mapped and prepared well ahead of the data room opening, which kept the process moving to terms both sides had already agreed in principle.

Pro tip from James Pugh: "Founders often prepare their pitch for the buyer and forget to prepare the evidence. By the time heads of terms are signed, your best-case story has already worked. What due diligence tests now is whether the underlying business matches it — so shift your energy from persuasion to proof."

Most due diligence problems are not dramatic. They are a pattern of small gaps that, together, undermine a buyer's confidence.

The most common in UK SME transactions: unsigned or informal contracts with major customers, intellectual property that technically belongs to a founder or contractor rather than the company, revenue that depends heavily on one or two accounts, and financial add-backs that cannot be evidenced with receipts or invoices.

None of these are automatically deal-breakers. A buyer can usually price around a known risk, or the parties can agree a warranty or indemnity to cover it. What buyers cannot price confidently is an unknown risk — something that surfaces late, unexplained, with no paper trail behind it.

That is the real cost of poor preparation. It is rarely the issue itself. It is the loss of trust that follows finding it.

A virtual data room is simply an organised, secure digital folder structure that holds everything a buyer's team will want to review. The details matter less than the discipline: consistent file naming, a logical folder hierarchy by category, and version control so nobody is working from an outdated document.

Founders who start this work 18 to 24 months before going to market are not doing so because CapEQ requires it. They are doing it because the alternative — assembling three years of documentation under pressure, mid-negotiation, while still running the business — is genuinely difficult to do well.

Preparation also changes who controls the narrative. A seller with an organised data room can present issues on their own terms, with context and a plan attached. A seller caught unprepared is explaining gaps reactively, often at the exact moment a buyer is deciding how much to trust them.

There is a practical benefit too, separate from trust. A data room that is tracked and indexed lets your adviser see exactly which sections a buyer's team keeps returning to. That pattern is useful information in its own right — it tells you where their concerns actually sit, rather than where they said their concerns sit during negotiation. An adviser can use that intelligence to adjust the conversation before a small worry hardens into a repricing demand.

None of this needs to happen all at once, and it rarely goes well when it does. Assign one person internally — often the finance director or company secretary — to own the data room as it builds. Treat it as a live resource, refreshed at least quarterly, rather than assembled once and left to go stale. Stale information causes almost as much friction in diligence as missing information, because a buyer has no way of knowing which version reflects the business as it actually stands today.

Due diligence typically opens once heads of terms are signed and runs in parallel with legal drafting of the sale and purchase agreement. For most UK SME transactions, the process itself takes between six and 12 weeks, though complex ownership structures, multiple entities, or contested IP can extend that considerably.

It rarely runs as a single, sequential exercise. Financial, legal, and commercial workstreams typically proceed at the same time, coordinated by the seller's advisers to avoid the buyer's team waiting on documents that should already exist.

This is also the stage where warranties, indemnities, and any retention or escrow arrangements get their final shape — each one usually a direct response to something diligence uncovered. The better prepared the data room, the fewer of these protective mechanisms a buyer feels they need.

It helps to think of diligence not as a single hurdle but as a staged release of information. Financial and commercial documents typically go first, since they carry the least sensitivity. HR, intellectual property, and other commercially sensitive material tends to follow once the buyer has confirmed genuine intent, often after an exclusivity period is agreed. A good adviser manages that sequencing on your behalf, so you are never disclosing more than the stage of the deal actually justifies.

What is due diligence in a business sale? Due diligence is the investigation a buyer carries out after heads of terms are signed, to verify the financial, legal, operational, and commercial claims made about the business before they commit to completing the purchase. It is the buyer's way of turning the seller's story into evidence they can rely on.

How long does due diligence take for a UK SME sale? Most straightforward SME transactions complete due diligence within six to 12 weeks, running alongside legal drafting of the sale agreement. More complex deals — multiple entities, disputed intellectual property, or regulatory approvals — can extend well beyond that, so an accurate estimate depends heavily on how prepared the seller's documentation already is.

What documents do buyers usually ask for? Buyers typically request three years of financial statements and tax records, signed copies of key customer and supplier contracts, the shareholder register and incorporation documents, intellectual property assignments, employment contracts, and a schedule of any current or historic litigation. The exact list is tailored to the sector and deal size, but these categories appear in almost every UK SME transaction.

What is a virtual data room? A virtual data room is a secure, organised digital repository where a seller stores every document a buyer's team needs to review during due diligence, structured by category with consistent naming and version control. It replaces the physical data rooms of previous decades and allows a seller's adviser to track exactly what a buyer's team has reviewed and where their attention is focused.

What are the most common due diligence red flags? The most frequent issues in UK SME diligence are unsigned or informal contracts with major customers, intellectual property registered to an individual rather than the company, revenue heavily concentrated in one or two customers, and financial add-backs that cannot be evidenced with supporting paperwork. None of these automatically end a deal, but each one typically slows the process and gives a buyer grounds to renegotiate terms.

Does preparing for due diligence increase my sale price? Preparation is best understood as protecting the deal you have already agreed, rather than manufacturing a higher one. A well-prepared data room reduces the chance of late-stage renegotiation, protects your timeline, and preserves the buyer's confidence — all of which matter more to the outcome than any single number.

James Pugh is a co-founder and Partner at CapEQ, who has personally advised shareholders on the sale of 50 privately owned businesses across consumer, retail, leisure, healthcare, and professional services.

James Pugh is a co-founder and Partner at CapEQ, who has personally advised shareholders on the sale of 50 privately owned businesses across consumer, retail, leisure, healthcare, and professional services.

He has advised founders through transactions including the sale of Liberty Flights to Supreme Plc, AV Danzer to the Wernick Group, and PayCaptain to The Citation Group

Related articles: