Discover the CapEQ approach to a premium exit

Whether you're exploring your options or fending off offers, we're here to help.

Selling a business is a once-in-a-lifetime decision, and these twelve avoidable mistakes quietly cost UK founders value, time and control.

Series: Business sale process · Business Sale Process Unpacked · Last updated: July 2026

The Gist

- Most owners sell a business only once, so the mistakes below are made fresh every time, by founders with every reason to know better.

- The twelve most common mistakes cluster around three themes: preparation, partners, and patience.

- Setting a minimum price before a proper valuation is one of the most frequent — and most costly — early errors.

- Approaching a known competitor first, without competing bids, is one of the surest ways to see an offer quietly eroded.

- A well-run process creates competitive tension between several credible buyers, rather than relying on the goodwill of one.

- The highest headline price is not always the best outcome once deal structure, warranties and payment terms are taken into account.

Few business owners get everything right first time when they sell a company. That is not a criticism — it is simply arithmetic. Most founders go through this process exactly once, while the buyer opposite may have done it a dozen times before.

Few business owners get everything right first time when they sell a company. That is not a criticism — it is simply arithmetic. Most founders go through this process exactly once, while the buyer opposite may have done it a dozen times before.

The most common missteps cluster around the same blind spots: unrealistic price expectations, misjudged buyer appetite, and the belief that a sale can be managed entirely alone, in the gaps between running the business. Here is our take on the twelve traps to sidestep, drawn from decades of partner-led mid-market M&A advisory work.

Each of these mistakes is avoidable on its own. Together, they explain most of the value that founders leave on the table — or lose altogether when a deal collapses.

Who would learn to drive without an instructor, or file a complex tax return without expert support? Plenty of people, it turns out. Read a few books, talk to a colleague, and cobble something together, telling yourself it can't be that hard.

In any complex situation — and an M&A transaction is necessarily multi-faceted — what you don't know matters more than what you do. Selling a business without an advisor is like climbing a mountain without an experienced guide. You may make progress, but never as much, and you take real risks along the way.

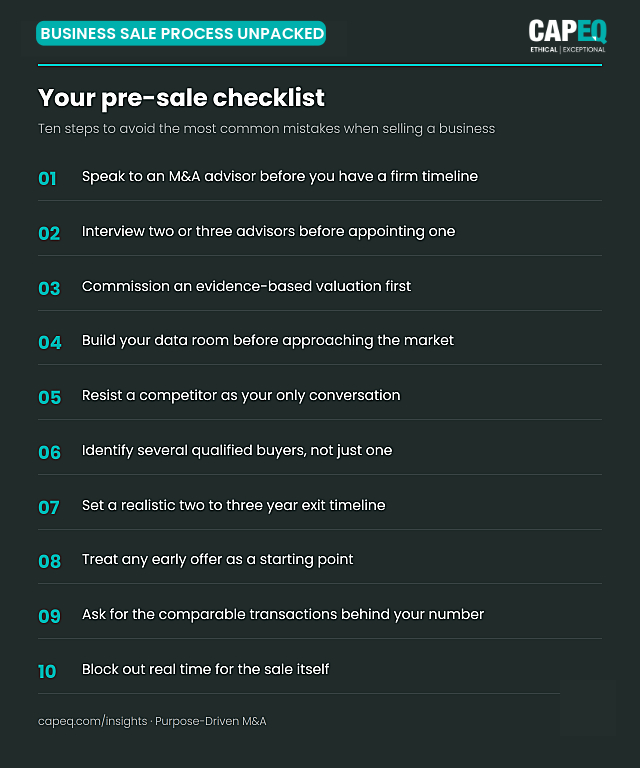

Avoid this by: speaking to an experienced M&A advisor early, even if you are years away from a sale.

Choosing the right adviser matters as much as choosing one at all. Appoint someone who has not completed multiple transactions before, and you will hit walls a more experienced advisor would have anticipated.

Look beyond experience, fees and accolades. Ask whether they feel right for you, whether they understand what makes your business yours, and whether they will still be picking up the phone at month nine of a nine-month process.

Avoid this by: interviewing two or three advisors and asking each how they would tell your story to a buyer.

It is normal, natural, and almost always a problem. By definition, you cannot know your price until a rigorous, evidence-based valuation is complete — one that reflects maintainable earnings, comparable transactions and buyer appetite, not hope.

Founders who fix a figure before the market has had its say tend to measure every offer against a target that was never grounded in evidence to begin with.

Avoid this by: working from an evidence-based valuation, not a hoped-for outcome.

It is tempting to talk up the business to support the number you want. That only works if every claim is backed by evidence a buyer can verify. Vague assertions — about recurring revenue, growth pipeline, or customer loyalty — end badly once due diligence begins.

An acquirer who loses confidence in your figures will price the uncertainty into the deal, loading risk back onto you, or walk away to a more transparent target. In any transaction that reaches completion, the truth surfaces eventually. Staying evidence-based from the outset is simply faster.

Pro tip from James Pugh: Build as much of your data room as you can before you go anywhere near the market, not once a buyer starts asking questions.

A business that can answer diligence requests within days, rather than weeks, keeps momentum — and momentum protects price.

Avoid this by: preparing your data room before you approach the market, not during diligence.

The most obvious buyer is often the person you already know — the one who has always wanted, or always competed for, your business. Surely it makes sense to approach them first?

Wrong, in almost every case. It is very hard to secure a defensible valuation from the first person you ask, especially someone you know well. They can make an agreeable offer over dinner, then quietly revise it down as they 'discover' unexpected realities, or manufacture them. With no competing bids to test the figure against, you are backed into a corner: take the reduced deal, or walk away with nothing to show for months of negotiation.

Avoid this by: running a structured process with several credible buyers from day one.

Businesses are often put up for sale at exactly the wrong moment — usually because of deteriorating financial performance, or personal pressure such as illness or divorce. Selling in a downturn is doubly hard: more businesses like yours are on the market, and fewer buyers are active.

Forced sales for personal reasons can feel unavoidable, but alternatives to a full exit often exist. Bringing in a strong management team can let a founder step back without selling outright — buying time to sell on their own terms later.

Avoid this by: planning your exit two to three years ahead, so you go to market on your terms, not the market's.

It can be tempting to accept an early offer, simply to avoid the time and emotional churn of running a full process. It is highly unlikely that anyone will pay over the odds without competitive pressure pushing them there.

A good M&A advisor holds the stress of a protracted process on your behalf, and creates the auction conditions that let you explore every credible option first.

Avoid this by: treating the first offer as the opening exchange, not the final word.

Value depends on comparable metrics: recurring revenue, market share, customer concentration, and adjusted profit margins. A surprising number of business owners have only a passing grasp of how these actually move a valuation.

An experienced advisor will show you the comparable transactions behind your number, so you are never simply taking someone's word for it. Without one, every offer becomes a matter of trust rather than evidence.

Avoid this by: asking your advisor to walk you through the comparable transactions behind your valuation.

Sometimes a sale genuinely must complete inside a fixed window, for commercial or personal reasons. Where that is the case, make the reasons clear to everyone at the table.

In every other scenario, there is little reason to self-impose a deadline. Move with purpose, but only as fast as is needed to do the job properly. A good advisor will explain why the timeline is what it is, and hold that pace under pressure from either side.

Avoid this by: agreeing a realistic timeline upfront, then revisiting it honestly at every stage gate.

In the run-up to exiting your business, it is essential to work on the sale, not just in the business. Owner-directors used to solving every problem themselves are often tempted to leave the process almost entirely to their advisor while keeping the day job going.

That instinct is understandable, but a sale still needs real engagement — for buyer meetings, management presentations, and the small decisions only the owner can make. Block out the time and treat the sale as the priority it is.

Avoid this by: delegating one significant operational area before the process starts, not partway through it.

The strongest transactions are built on shared understanding, not persuasion. Keep asking questions, both to sharpen how you position your business and to understand each bidder's motivation and real areas of concern.

The more you listen, the more you learn about what actually matters to the buyer — and the better positioned you are to close gaps before they become sticking points.

Avoid this by: going into every meeting with three open, genuinely curious questions prepared in advance.

Few of us are wholly dispassionate about a transaction that represents years, or decades, of our working life. Passion is natural. Overused, it becomes counterproductive.

Founders can lock onto a position and find it hard when their assumptions or figures are challenged. Ultimatums get issued. Positions harden. Anyone who declares 'the deal is off unless we hit this number' tends to lose their buyer, alienate them, or block a compromise that would otherwise have closed the gap.

This is why an advisor's temperament matters as much as their technical grasp of the numbers. By keeping talks level-headed, an experienced negotiator can stop a deal running aground over a point that, three weeks on, nobody remembers arguing about.

Avoid this by: agreeing your walk-away position privately with your advisor, and trusting them to defend it on your behalf.

Every mistake above becomes less likely, or less costly, when a sale is run as a structured process rather than an improvised one. The table below sets out how the two approaches typically compare.

| Stage | Going it alone | Structured, partner-led process |

|---|---|---|

| Valuation | Owner's own estimate, often anchored too high or too low | Evidence-based valuation using comparable transactions |

| Buyer pool | Usually one known contact, approached first | Several qualified, credible buyers approached in parallel |

| Negotiating leverage | Limited, since there is nothing to compare an offer against | Competitive tension between bidders supports the price |

| Due diligence | Documents assembled reactively, under time pressure | Data room prepared in advance, reviewed before it is needed |

| Owner's time | Founder manages both the business and the deal alone | Advisor absorbs process load; founder stays focused on trading |

| Outcome | Often the first credible offer, taken to end the strain | A chosen offer, weighed against real alternatives |

A significant number of CapEQ clients arrive for a first conversation having already had one of these mistakes cost them time, momentum or leverage. None of them are unusual founders — they are simply doing something once that the buyer opposite has done many times before.

Use this in the months before you go to market. It mirrors the twelve mistakes above, turned into practical steps.

The single most common mistake is treating the sale as something to manage alone, in the margins of running the business, rather than as a structured process in its own right. This tends to compound every other mistake on this list, because there is no experienced advisor to catch each one before it affects the outcome.

Ideally, two to three years before you plan to exit. That gives enough time to build an evidence-based valuation, resolve documentation gaps, and reduce dependency on the owner. Preparation started this early rarely goes to waste even if plans change, since a well-run business is easier to lead as well as easier to sell.

Not as your only conversation. A known competitor can be a genuine buyer, but approaching them exclusively removes competitive tension from the negotiation, and offers are far more likely to be revised downward once you have no alternative to compare them against. It is usually stronger to run a structured process with several qualified buyers, even if that competitor remains one of them.

Sales most often stall or collapse when due diligence uncovers gaps between what was claimed and what can be evidenced, or when the owner has not made real time for the process alongside running the business. A well-prepared data room and a realistic, mutually agreed timeline are the strongest protections against a deal losing momentum.

No. Deal structure matters as much as the number: payment terms, warranties, earn-outs and any conditions attached to completion can all change what a founder actually receives, and when. A lower headline offer with cleaner terms and faster certainty of completion is often the stronger outcome once the whole package is compared.

It is possible to sell without one, but it materially increases the risk of the mistakes above, from an unevidenced valuation to a negotiation with no competitive tension behind it. An experienced, partner-led advisor brings a structured process, a qualified buyer pool and the temperament to hold difficult conversations on your behalf.

James Pugh is a co-founder and Partner at CapEQ, the Certified B Corporation lower mid-market M&A advisory. A multi-exit entrepreneur before moving into advisory work, he has led transactions across consumer, retail, leisure, healthcare and professional services, with more than 50 completed deals to date.

James Pugh is a co-founder and Partner at CapEQ, the Certified B Corporation lower mid-market M&A advisory. A multi-exit entrepreneur before moving into advisory work, he has led transactions across consumer, retail, leisure, healthcare and professional services, with more than 50 completed deals to date.

Read his full bio or book a confidential chat.