Discover the CapEQ approach to a premium exit

Whether you're exploring your options or fending off offers, we're here to help.

Valuation methods set the range. Competitive tension sets the price. Here is how business valuation actually works in mid-market M&A.

Series: M&A Valuation Drivers · Part 1 of the series · Last updated: 15 May 2026

The Gist

- There are four main methods to value a business: EBITDA multiple, discounted cash flow (DCF), asset-based, and revenue multiple. Most professional valuations use two or three and triangulate.

- Methods give you a range. They do not give you a price. The price is what the right buyer will pay in a competitive process.

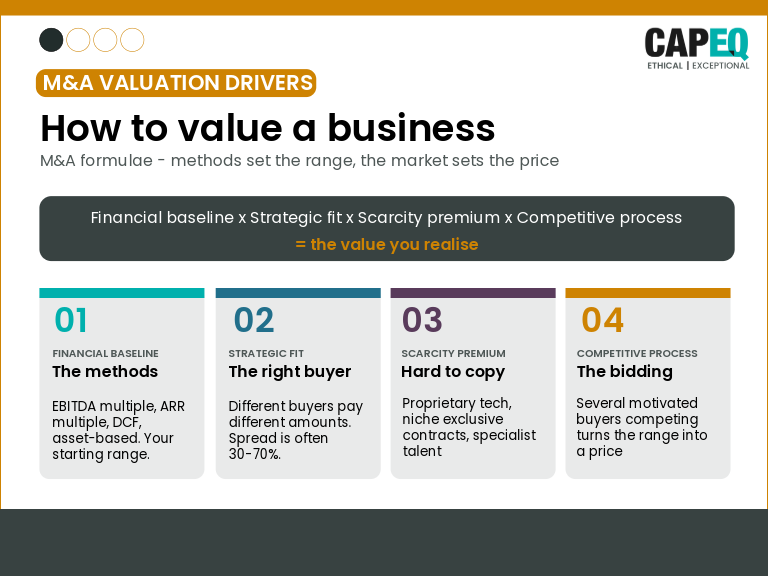

- The CapEQ formula: Financial baseline × Strategic fit × Scarcity premium × Competitive process = the value you realise.

- We do not put a number on your business before taking it to market. A pre-valuation either anchors low and short-changes you, or anchors high and sets you up to fail. Neither serves you.

- Below: the four methods explained, three real deals where the market revealed value, and a checklist you can use today.

To value a business, work out what it earns, apply the right method for your sector (most UK mid-market deals start with an EBITDA multiple), then adjust for risk, growth, and what makes your business hard to replace. That gives you a range. The actual price is what the right buyer will pay when several bidders are competing — which is often well outside the range any one valuation method produces. That is why a single number, calculated in advance, is a fiction.

We have all been there. A founder mentions to a friendly accountant that they might be thinking about a sale in a year or two. The accountant runs a quick EBITDA times multiple, sends a number back, and the founder builds their retirement plan around it.

Sometimes the number is roughly right. Often it is not. And when it is wrong, it is wrong in ways that cost you.

A pre-valuation does one of three things: it anchors you too low and you accept the first offer that clears the bar; it anchors you too high and the process drags on until your business looks tired; or it points at the wrong type of buyer entirely. None of those outcomes is what you want.

At CapEQ, we deliberately do not put a number on your business before taking it to market. That is not us being coy. It is us being honest: until the right buyers have looked, met you, modelled the deal, and competed for it, nobody knows what your business is worth. Including us. Including you.

What we can do is show you how the methods work, where your business sits inside the range each method produces, and how the gap between the range and the realised price is closed by a properly run competitive process.

Most UK mid-market valuations use a blend of the methods below. None of them is perfect. Each tells you something different. A good adviser will use at least two and explain why one is more relevant for your business than the others.

| Method | What it measures | Best for | Typical UK range |

|---|---|---|---|

| EBITDA multiple | Profit before interest, tax, depreciation, and amortisation (EBITDA), multiplied by a sector benchmark | Established trading businesses with stable earnings | 4–8× EBITDA for most; higher for technology, and healthcare |

| Discounted cash flow (DCF) | The present-day value of forecast future cash flows | Businesses with strong, predictable cash flows and credible forecasts | 12–18% discount rate for an established mid-market business |

| Asset-based | Fair-market value of tangible and intangible assets minus liabilities | Asset-heavy businesses (property, plant, stock); or as a floor check | Lowest of the four; useful as a sanity check |

| Revenue multiple | Annual recurring revenue (ARR) multiplied by a sector-specific factor | Pre-profit, fast-growing, or recurring-revenue businesses | 0.5–3× revenue for most; higher for high-growth SaaS and AI scale-ups |

A fifth approach, the rule of thumb or industry shorthand (for example, high street accountants at roughly 1× annual fee income, pharmacy prescriptions issued per month), is useful for framing the value-add. It should never be a primary method. As the team at American Business Appraisers put it, valuation needs cash-flow thinking and proper risk analysis; a quick rule of thumb cannot capture that. Eqvista makes a similar point about UK businesses: rules of thumb are reasonableness checks, not conclusions.

EBITDA is the closest thing the M&A world has to a common language. It strips out the things that vary by ownership structure (debt, tax position, depreciation policy) and gives buyers an apples-to-apples view of the business's underlying profitability.

A founder-run business with £1.5m of EBITDA and a "messy" set of accounts will typically attract a different multiple from a business with the same EBITDA, clean accounts, recurring revenue, and a management team in place. The multiple range is wide for a reason.

Worked example. A B Corp-certified food manufacturer with £1.2m EBITDA, in a growing category, with retained management and contracted supply agreements. Sector multiples in mid-market food and beverage have ranged from 5× to 9× in recent UK deals. The EBITDA method gives a range of £6m–£10.8m. That is the floor of the conversation, not the ceiling.

DCF projects free cash flow for five to seven years, applies a terminal value beyond that, and discounts the lot back to today's money using a weighted average cost of capital (WACC). Harvard Business School calls it the gold standard.

It is also dangerously sensitive to assumptions. Change the discount rate by two points or the terminal growth rate by one, and your number moves by 20–40%. Use DCF as a cross-check on EBITDA multiples, not as a standalone answer. And be wary of any adviser who builds a DCF on aggressive forecasts they cannot defend.

The asset approach values everything on the balance sheet at fair-market value, subtracts liabilities, and stops there. It is the right method when assets are the business (property holdings, equipment hire, stock-heavy distributors) or when the business is being wound up.

For an ongoing, profitable trading business, asset-based valuation almost always understates the price a buyer will pay. The reason is goodwill — the value of customer relationships, brand, know-how, and people that does not show on a balance sheet. Use asset-based as your floor, not your starting point.

For early-stage and pre-profit businesses, especially in software-as-a-service (SaaS), e-commerce, and life sciences, profit is a misleading number — these businesses are deliberately reinvesting every pound into growth. Revenue multiples are the workaround.

Multiples vary wildly by sector and growth rate. A SaaS business growing 40% a year with 90% gross-revenue retention will attract a very different multiple from a flat-line agency on the same revenue. Use revenue multiples for the right businesses, then cross-check against forecast EBITDA in two to three years' time.

Once you have a range from the methods, you need a way to think about how the range becomes a price. Here is ours:

Financial baseline × Strategic fit × Scarcity premium × Competitive process = The value you realise.

The first factor is what the methods give you. The next three are where most of the value lives, and where a partner-led process makes the difference.

A single number, calculated in advance, captures none of the multipliers. That is why we hold our nerve and refuse to give one.

Factmata, a UK AI start-up specialising in social-media risk detection, had what most acquirers wanted but could not build quickly — proprietary AI for misinformation detection, a niche position, and seven developers who knew the domain. We ran a process that put that scarcity in front of strategic buyers globally.

Cision, the Chicago-headquartered media-intelligence leader, acquired the business and redeployed the engineering team into its AI roadmap. Setting a valuation before going to market would have undervalued the business by a wide margin. The scarcity premium did the work, and the competitive process realised it.

Takeaway: When your value sits in intangibles, multiples are the floor. The right strategic buyer pays for what they cannot replicate.

Three patterns we see again and again.

We are partner-led mid-market M&A advisers. We are also an accredited B Corp. That combination is deliberate: we believe a sale process should secure the maximum defensible valuation and the right home for what you have built.

When you work with us, you get a clear view of the methods, the range, and the realistic strategic-fit multipliers in your sector. You get a buyer list that goes beyond the obvious. You get a process that creates competitive tension. And you get partners who have done this for decades, alongside you for every conversation.

What you do not get is a number on day one. By the time we are talking, you should know why.

How do I value my business quickly? Take a normalised EBITDA from your last full year, apply a typical multiple for your sector (4–8× for most UK mid-market), and treat the result as the bottom of a range. For a more accurate view, you need a proper analysis of cash flow, growth, customer concentration, and sector dynamics.

What is a good EBITDA multiple for my business? The honest answer is: it depends. Sector, size, growth rate, customer concentration, recurring revenue, management depth, and current M&A market conditions all move the multiple. A specialist adviser will give you an evidence-based range rather than a single number.

Why does CapEQ not provide a valuation upfront? Because we believe a single pre-market number does more harm than good. It anchors expectations and steers the process. The real price is revealed by the right buyers competing, and we get there with you rather than guessing in advance.

How long does a business sale take? Six to twelve months is typical for a sub-£100m deal, from first conversation to completion. Preparation can take longer, especially if the business needs management depth, data, or contracts tidied before going to market.

Do I need a formal valuation report? Only for specific purposes: tax, divorce, shareholder dispute, employee share scheme, or buy/sell agreement. For a sale, you want a market-tested price, not a desk-based number.

What is the difference between enterprise value and equity value? Enterprise value is the value of the whole business, debt-free and cash-free. Equity value is what you actually receive — enterprise value adjusted for surplus cash, debt, and working capital. A £10m headline is rarely £10m in your bank account.

Douglas Edmunds is a Partner at CapEQ with 10+ years of M&A experience. He has led sell-side and buy-side mandates across technology, healthcare, industrial, and consumer sectors. CapEQ is a Certified B Corporation.

Douglas Edmunds is a Partner at CapEQ with 10+ years of M&A experience. He has led sell-side and buy-side mandates across technology, healthcare, industrial, and consumer sectors. CapEQ is a Certified B Corporation.